Karen Tang, CFP®: Certified Financial Planner in Singapore

Life Stage Planning – Make Financial Planning Part of Life Planning

Just like how financial markets fluctuate, your finances and financial needs will also change with time. Fortunately, it is easier to predict the changes in your financial life stages than it is to predict the direction of the markets.

Generally, most people pass through three primary financial life stages as they age. While not exactly unpredictable, family circumstances, financial issues and considerations, income levels, cashflow and spending habits tend to follow a pattern at each of these life stages.

What is Life Stage Planning?

It is the approach where financial objectives at each life stage are identified and appropriate strategies and plans are recommended to meet these objectives.

The financial planner needs to ensure that strategies and solutions are suitable and cost effective, and they continue to be advantageous and relevant throughout the life cycles.

The right solutions will ensure that gaps are closed and in the case of insurance, the financial planner must ensure that necessary protection is secured before any ill health sets in, making the client uninsurable. Hence, taking the right action at the right time is vital.

What is Your Current Life Stage and Circumstances?

Financial planning is a continuous and dynamic process. It is highly advisable that you meet up with your financial planner to review your financial plan at least once a year.

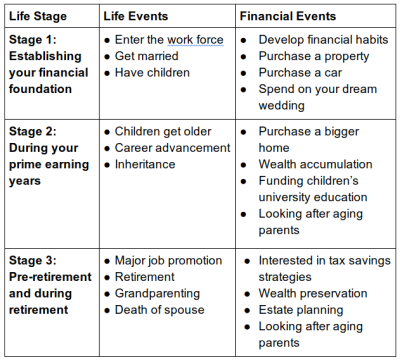

The table below gives you a general idea of the events that are likely to take place at the different life stages.They are by no means exhaustive. What each major life event requires you to do is size up its financial impact and then do what is possible to prepare for the consequences.

Stage One: Establishing Your Financial Foundation

Young working adults have few or zero assets and some would have instalments like student loans to pay off. A big part of their income is used to cover living expenses, with little left to set aside as savings. They face the task of learning how to manage spending and saving within the constraints of their income levels.

Developing sound financial habits is critical at this stage as this will have an impact on their money management in the future.

The main concern here is what if a major illness, disability or premature death strikes. They need to ensure that they have adequate insurance coverage. The other important thing that young working adults should do is to start a regular savings plan (RSP). Car and home ownership are big asset items, hence, it is important to plan for them.

Here are some practical ways to help build a solid financial foundation:

1. Track your spending habits to identify ways to save

Use a budgeting and spending app to help you. Once you get the hang of it, you will be surprised at how easy tracking your expenditure can be and the clarity it gives you.

2. Set aside 3 to 6 months of expenses as emergency funding in a savings account

These funds can protect you against unforeseen events such as loss of employment.

3. Pay your credit card bills on time and in full

This can not be emphasized enough. Be clear about ‘needs’ and ‘wants’. Weigh your options instead of buying on impulse.

4. Put in place a saving ‘ritual’

If you are not a disciplined saver, consider an automatic savings program so that a portion of your monthly pay cheque is deposited into a separate savings account. This is a ‘no brainer’ and you do not feel the pinch nor do you have to make a decision how much to save.

5. Set savings goals

Try this out because I have seen it work successfully with many people. Whether you want to accumulate a down payment for a property or pay for a month long overseas vacation, when you connect a tangible goal with your saving ability, it provides the motivation and discipline you need to achieve your goals.

6. Be adequately insured

Make sure you have sufficient and the right type of insurance coverage to protect yourself and your family.

Stage Two: During Your Prime Earning Years

This is often a time when you are at the peak of your career, where your income level is increasing. A higher disposal income also means increased spending. More comfortable homes, bigger cars and raising children can all easily deplete your income. Efforts must be made to save diligently and invest for children’s university education and to prepare for retirement.

This is also the time when the financial decisions you make will have the greatest impact on your retirement lifestyle and financial health. By now, you should have a healthy bank account and be able to make well informed financial choices.

1. Start early to save for children’s university education

Time is your best friend. The earlier you start, the less you have to set aside each month.

2. Invest wisely

Consider an asset allocation strategy that matches your time horizon and risk tolerance. Have regular conversations with your financial planner and rebalance your portfolio whenever necessary.

3. Plan for your retirement income

Consider your streams of income during retirement. Understanding what your retirement lifestyle would look like is the first step in determining the income that you need. Be realistic and be kind to yourself. Do not under estimate your living expenses – you are ‘on holiday’ every day and this requires money. Don’t forget to factor in your insurance premiums as well as inflation.

4. Make sure your insurance protection has kept pace with your needs

Having adequate life insurance and the right type of insurance are crucial. Mortality or death insurance is critical when you have a family and dependents to provide for in the event premature death.

5. Make sure your spouse and children are adequately covered by the right type of insurance

A health crisis can happen to anyone in the family and it can exhaust your savings. A home maker spouse needs to be insured and so do children. Do not be penny wise pound foolish.

6. Plan for the cost of caregiving of your parents

This contingency amount needs to be factored into your financial plan well in advance. There are ways in which you can mitigate caregiving risk.

7. Prepare an estate plan

This is to ensure that your custodial, financial and medical wishes are carried out. For parents with children who are minors, getting a will done is extremely important as you need to give instructions regarding guardianship. Other common estate planning tools include trust, lasting power of attorney and advanced medical directive.

Stage Three: Nearing or During Retirement

The main concern is whether you can be financially independent and ideally depend on passive income for your retirement needs. WIth increasing longevity, it is prudent to include a buffer in your retirement planning so that you do not outlive your resources.

Annuities and retirement income plans are relevant solutions to consider. If you have a Supplementary Retirement Scheme (SRS) account, you can withdraw the money over ten years from age 62 to 72. If you have a lump sum pension or gratuity, it is important to invest the money in low risk instruments, preferably with some form of guarantee.

If you had planned well, the high medical expenses expected in old age would be adequately taken care of by health insurance which you had taken up earlier. Always renew your medical insurance on time to avoid a policy lapse. The last thing you want is to be left stranded without any coverage because of your uninsurability.

Those who are financially well endowed will need to do estate planning to ensure that their wealth is passed on efficiently and legally. Wills and trusts are two common estate planning tools. Work with a qualified estate planner to ensure that your last wishes are properly documented.

These years can and should be some of the most enjoyable and fulfilling times of your life. If children and grandchildren are part of your life, having the financial ability to help them can be rewarding.

Here are some key things to note and take necessary action if need be.

1. Ensure your health insurance is adequate

Health care cost in Singapore continues to rise and we are living longer. Private health insurance will be important as it is more comprehensive than the basic MediShield Life cover.

2. Get Long-Term Care insurance

This is to protect your hard earned retirement savings. You do not want a severe disability to wipe out your entire life savings.

3. Update your estate plan

Changes in your financial and family situations should be triggers for reviewing your estate plan with a qualified estate planning professional.

4. Manage your investments cautiously

You should be in wealth preservation mode. If you have a financial planner or broker managing your investments, be sure to get regular updates from him. Understand the consequence of your investment decision. When in doubt, ask questions. If you do not feel completely comfortable with a recommendation, do not proceed.

5. Enjoy your truly “golden” years!

A successful career, the freedom to live the lifestyle of your choice and a sense of satisfaction with what you have accomplished can make your “golden” years truly enjoyable.

Every individual is different. While the broad principles are the same, the application of the principles, strategies and solutions differ.

It is important that your financial plan is well conceived, robust and executed properly. It is also equally important to monitor, review and reshape the plan as you progress in it.