Karen Tang, CFP®: Certified Financial Planner in Singapore

How does CareShield Life affect me? Should I switch to CareShield Life or stay put with ElderShield?

In my previous article, I shared what one needs to know about CareShield Life, especially for those turning age 30 to 40 in 2020. This new and improved national scheme that replaces ElderShield was officially launched on 1 October 2020.

Who does CareShield Life cover?

Singaporeans born in 1980 or later (aged 30 to 40 in 2020):

CareShield Life is compulsory for all Singaporeans aged between 30 to 40 in 2020 and enrolment is automatic. This is regardless of any pre-existing medical conditions and disability. This ensures that young Singaporeans have some form of basic protection for long term care.

If you are born after 1990 (aged below 30 in 2020), you will be automatically covered when you turn 30. You will receive a letter about 2 months before your 30th birthday, and premiums will be made available closer to your 30th birthday.

What about those who are older?

Singaporeans born in 1979 or earlier (aged 41 and above in 2020):

- Your current ElderShield plan will continue to protect you.

- Participation is optional. You can choose to join CareShield Life from end 2021 onwards if you are not severely disabled. There is no maximum entry age. More information on how to apply will be provided closer to the end 2021.

- Those who have opted out of ElderShield can opt into CareShield Life if they are currently not disabled.

- Those born between 1970 and 1979 (aged 41 to 50 in 2020), and those who are currently insured under ElderShield 400 and not severely disabled, will be automatically transitioned to CareShield Life from the end of 2021.

- However, you can choose to opt-out by 31st Dec 2023 if you do not wish to remain on CareShield Life. More information on auto-enrolment will be provided closer to end 2021.

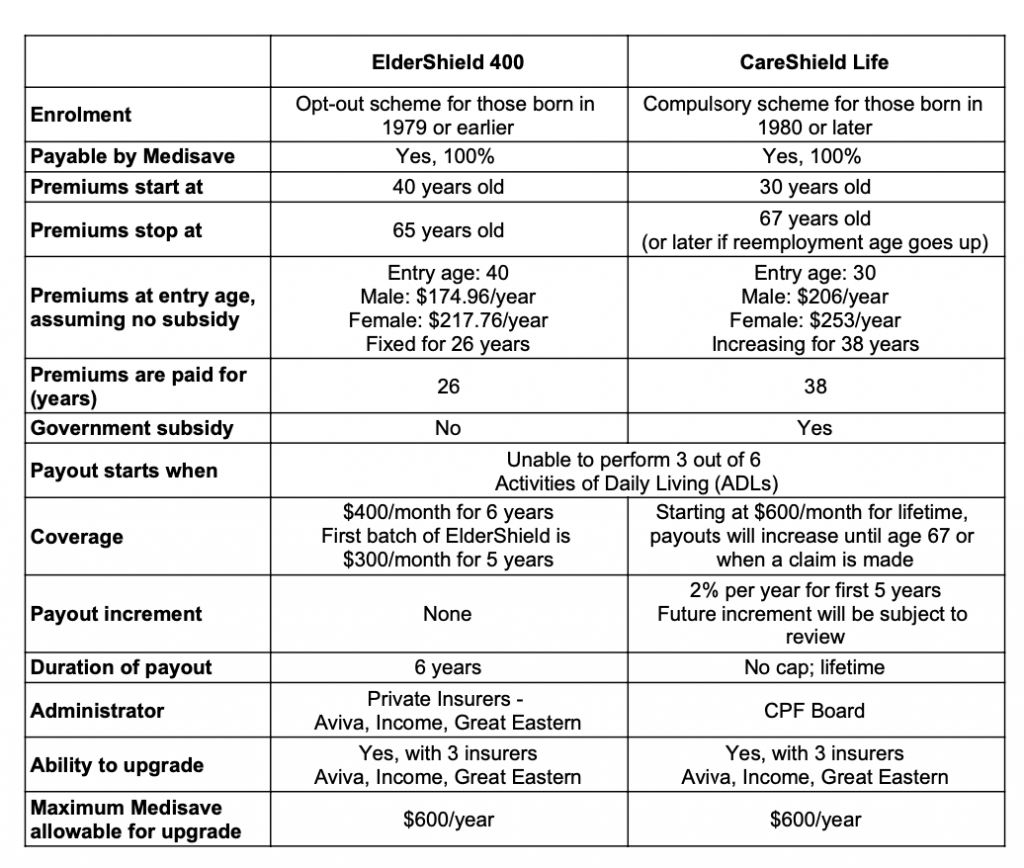

Differences between ElderShield and CareShield Life

Before you decide whether CareShield Life is a suitable option for you, let’s take a look at the differences between these two schemes.

What about Premiums?

Premiums of CareShield Life are higher than ElderShield. For example, a male who enrolled to the current ElderShield scheme at the starting age of 40 pays $175 per year while the CareShield Life premium for a 40-year-old is $318 per year.

Just like how CareShield Life’s payouts increase by 2% over time (up till the time of claim or age 67 whichever is earlier), premiums also go up by 2% per annum for the first 5 years. The rate at which it will increase in subsequent years will be decided by an appointed council.

The Government will provide subsidies for switching over from ElderShield to help you manage the increase. But bear in mind this is at best ‘transitional’ and not permanent.

It is useful to calculate the ‘coverage to premium ratio’ or what we call a cost benefit analysis. This will serve as a guide in helping one decide whether it is better to switch over to CareShield Life or not.

So, how will CareShield Life affect me?

That depends on which group you fall under. If you are aged 40 and above this year, you will likely fall under one of the 3 categories below.

Group 1: You are on the basic ElderShield scheme, without any ElderShield Supplement

You were automatically enrolled in ElderShield and are paying premiums through Medisave. You did not enhance the monthly payout with a Supplement offered by one of the 3 appointed private insurers, namely Aviva, NTUC Income, and Great Eastern. Depending on your age, you are either covered under ElderShield 400 which gives a payout of $400 per month for 6 years or under ElderShield 300 that pays $300 per month for 5 years in the event of severe disability.

Group 2: You have an ElderShield Supplement

On top of ElderShield, you have an ElderShield supplement. This Supplement provides you with a higher monthly payout and an extended payout duration.

Group 3: You are not on basic ElderShield

You may have previously opted out of ElderShield or were unable to get coverage because of pre-existing medical conditions. Or you could be someone who turned 40 years old before the ElderShield scheme started in 2002. In this case, making the switch to CareShield Life will be beneficial as you are able to enhance your insurance coverage. Do note that the switch is only possible if the existing ElderShield policyholder is not already severely disabled.

If you are not sure which category you belong to, you can log in to the CPF website to check (under the Health section).

For existing ElderShield policyholders:

- You will have an option to switch to CareShield Life from 2021 to get the enhanced benefits.

- Upon switching, ElderShield 400 policyholders will pay a base CareShield premium depending on your age.

- ElderShield 300 policyholders and those not currently insured by ElderShield will need to pay an additional catch up the component for the 10 years.

- You can also choose to maintain the status quo and remain on the ElderShield scheme.

In that case, you will continue to get the same benefits and pay the same premiums.

To switch or not to switch?

There is no right or wrong answer. It depends on your preference and circumstance.

- Preliminary findings reveal that it is more cost effective for you to remain on the ElderShield scheme. Not only is the basic ElderShield plan cheaper than CareShield Life, the ElderShield supplements are also priced more competitively.

- If you are currently on a basic ElderShield scheme and do not intend to get an ElderShield Supplement, then CareShield Life’s incremental coverage, and especially its lifetime payout structure may be useful.

- If you already have an existing ElderShield supplement that pays you a much higher payout for example, $2,000 or more per month for a lifetime, then the increase in Careshield Life benefits may not be very significant compared to what you already have.

More important than switching …….

Take action today to enhance your ElderShield coverage with an ElderShield supplement.

It is clear that payouts from both CareShield Life and ElderShield are unlikely to sufficiently provide for peace of mind when the loss of independence happens. Hence, it is important for you to put in place your own plans that are tailored to your needs and expectations.

In my article “Are you turning age 30 to 40 in 2020? Here’s What You Need to Know about CareShield Life.”, I had shared with you that the average cost of care for disability is close to $2,400 per month.

By upgrading your existing ElderShield coverage first to the level of coverage you want, you can immediately enjoy the enhanced coverage and payout period as well as ‘lock-in’ your good health. Even if your health status changes, later on, you are already well covered without the need to switch to CareShield Life. For a start, consider upgrading your long-term care insurance coverage to $2,400 a month in payout should loss of independence happen.

Do a review with your financial planner to decide on the most appropriate option for your needs. If you do not have a trusted financial planner to guide you, reach out to me for a discussion.

Insurance is such – it is better to have something and not need it than to need something and not have it. The impact of whether you are sufficiently insured may be the difference between financial independence or financial disaster.

Continue to stay safe and healthy!