Karen Tang, CFP®: Certified Financial Planner in Singapore

A well deserved, comfortable retirement is what we all look forward to in our golden years. Needless to say, the stakes are high and any mis-steps along the way can cause our plan to derail – from independence, joy and freedom to poverty, dependence, and penny pinching. For a financially worry-free retirement, you need to avoid these costly mistakes.

Retirement Planning Mistake #1: No Plan in Place

This is the mistake most people make. Failing to plan is as good as planning to fail. The sad truth is most people spend more time planning their vacation than their financial future! Saving blindly for retirement will not help. You got to have a plan, my friend.

- Set specific, measurable and attainable financial objectives in writing.

- Commit to and implement a step-by-step action plan to achieve financial success.

- Review your asset allocation, investment performance and total savings on a regular basis and make changes whenever necessary so that you leave nothing to chance.

People who had formal retirement planning done through a professional financial advisor have much more financial success than those who did not. If you do not have a plan in place yet and need retirement advice, feel free to reach out to me.

Retirement Planning Mistake #2: Don’t Save Enough

Examine your expenses and spending habits. Look for alternatives. Redirect your priorities. A sufficiently funded retirement requires an unwavering commitment. When there is a will, there is a way!

What is the opportunity cost of current consumption?

Saving for retirement is about priorities and alternatives. Do you upgrade your car to the latest model now or stretch its life with a few repairs so you can enjoy a more enriching retirement lifestyle? How about forgoing that Rolex watch now and go with a less costly option so that you can buy a little more comfort in retirement with the difference?

The choices you make today will have significant implications for the last 30 to 40 years of your life. And sometimes, it is the little things that can add up to a sizeable amount.

Take for example: What is the real impact of buying that one cup of artisanal coffee everyday?

Let’s say it costs SGD$5.00 per cup and you have one everyday. Multiply this by 20 days per month, for say, 40 years at 6% interest and it compounds to an astonishing $185,714 that could be saved for retirement! How about getting an espresso machine at home and you be your own barista for a couple of minutes to prepare your coffee? It is a small price to pay for that added security in your retirement.

And that is just coffee – imagine all the other areas where your current consumption could be redirected to savings. It may seem tough at first but when you see the result of more savings in the bank, you will find this habit pretty addictive.

Increasing life expectancy

Singaporeans are already enjoying a higher average lifespan. This means you need to plan your retirement even more carefully so as not to outlive your savings. One way to find out how much to save is to evaluate what your ideal retirement will be like.

According to a Manulife survey, investors expect their retirement expenditure to be 64 percent of their current expenditure. In reality, however, retirement expenditure may even be higher than their current expenses.

Saving for retirement

Can you exchange instant gratification for delayed consumption so that you can enjoy a truly golden retirement later?

Think long term. It’s not how much money you make that determines your financial success, but what you do with what you make. Your habits will determine your success.

The bare minimal that everyone ought to save is 10% of their take home salary. However, if you factor in inflation, debts, and a retirement vision that includes travelling abroad 3-4 times a year, giving to charity and fulfilling other dreams, then saving just 10% will not cut it.

Clearly, the lesson here is to start saving for retirement early – and save aggressively. Every day you delay just raises the percentage of income you must save and increases the leverage and risk required to achieve the same financial goal. There is an easy way and a hard way to save for retirement, and the easy way is to start early and save aggressively.

What percent of your income is being saved? Is it enough?

If you need help figuring out your retirement plan, come talk to me. Don’t leave your retirement to chance!

Retirement Planning Mistake #3: Not Starting to Save Early Enough

It is not money that builds wealth. It is Money x TIME = Wealth. For compounding to work its magic, you’ve got to give it time. The longer you delay, the harder it is to save as your mortgage or your children’s needs take priority. Procrastination is an expensive mistake that should be avoided at all costs!

When is a good time to start saving for retirement?

As soon as you start work as a young adult! Why? Because the earlier you start, the lower the cost towards building your retirement nest egg and the closer you get to achieving your desired goals. Unfortunately, this is rarely a financial priority for young adults as wedding expenses and buying the matrimonial home would have taken up a huge chunk of their savings.

Well, all is not lost – the important thing is to start. The amount set aside may be small in the beginning but it can increase over time as you progress in your career. Work with a qualified financial planner so that you will have a comprehensive perspective of your retirement planning.

Procrastination can jeopardise your retirement

When you are still in your 20s or even 30s, retirement may seem too far away in the future to think about. Because of this, we end up putting off planning and saving for retirement.

What many fail to realise is that it is easier to contribute to your retirement plan when you still have very few financial responsibilities. It may be more difficult to save for your retirement when you are already supporting children and ageing parents, and paying for a house and a car.

Moreover, the earlier you start contributing, the more time you have for compounding to increase your money. Last minute contributions have less time to compound.

Another fact that most do not understand is this: If you start desperately trying to amass a retirement nest egg at the age of 50 (which is extremely late!), you will have to fork out a high 6-figure sum or even a million depending on how much you want as retirement income.

It is clear that many Singaporeans think they have all the time in the world to start planning for retirement, based on the fact that one-third of working adults are not planning for retirement, and of those who are, 6 out of 10 people start saving for retirement only at age 45. Starting late is the main reason people can’t retire comfortably – not earning too little.

The Miracle of Compounding

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” Albert Einstein

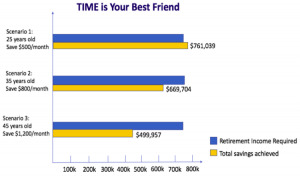

The chart below illustrate three different scenarios:

- Scenario 1: You start saving $500 every month from age 25, with returns of 5% compounded annually until age 65.

- Scenario 2: You start saving more at about $800 every month from age 35 with same returns of 5% compounded annually until age 65.

- Scenario 3: You start saving even more at $1,200 every month from age 45 with returns of 5% compounded annually until age 65.

Which scenario do you think will have the most retirement savings?

As you can see, you would have the largest nest egg if you started saving at age 25, despite setting aside the smallest amount each month.

This can happen because of compounding interest.

Compounding, simply put, is interest earning interest. It is the exponential increase in your investment where interest is earned upon your principal and the accumulated interest. Given time, compounding is the most fundamental way to build wealth.

Retirement Planning Mistake #4: Relying On Central Provident Fund (CPF)

Realistically, payouts from the CPF Life plan are insufficient to meet your retirement funding. It provides only a small fraction of funds needed in retirement and yet, many are heavily dependent on this source of savings to fund their retirement.

To give you an idea of the payouts from the 3 different CPF Life Plans:

John has turned age 55 and he has chosen to set aside the Full Retirement Sum of $166,000. He would like to start receiving payouts at age 65.

- Standard Plan (more for self) – $1,253 – $1,375 monthly payout

- Basic Plan (more for loved ones) – $1,142 – $1,256 monthly payout

- Escalating Plan (more for the future) – $984 – $1,090, increasing at 2% every year

As John is married with a 3 year old daughter, he wants to leave some cash for them upon his demise (also called a bequest). Hence, the Basic Plan is most appropriate for him.

So, If you are in John’s position and you have opted for the Basic Plan, do you think $1,256 per month is adequate to support your retirement lifestyle?

Clearly, you need to plan for other sources of retirement income. And always plan for more than the bare minimum because each day in retirement is a holiday and when on holiday, we spend more.

Learn more about the other pitfalls of retirement planning at ‘Secure A Comfortable Retirement by Avoiding These 12 Mistakes – Part 2’.