Karen Tang, CFP®: Certified Financial Planner in Singapore

Are you turning age 30 to 40 in 2020?

Here's What You Need to Know about CareShield Life

The much-awaited CareShield Life is launched today, 1 October 2020. I have been getting some questions about this improved version of the ElderShield plan. And I thought it would be helpful if I could share with you what CareShield Life is, its features, and how you can benefit from it.

If you are turning age 30 to 40 in 2020, this article is for you as you will be the first cohort who will be affected. Come 1 October 2020, all Singaporeans and PRs turning age 30 to 40 will be automatically enrolled in CareShield Life and participation is compulsory.

What is CareShield Life?

CareShield Life is the new national long-term care insurance scheme for all Singapore Residents born in 1980 or later, including those with pre-existing disabilities (for those born in 1979 or earlier). It is an improved version of the ElderShield plan. A significant enhancement is that it provides lifelong cash payouts, which in turn gives greater assurance for basic long-term care needs.

What is Long-term Care and Why is it Important to Me?

Long-term care is the help you will need with daily tasks like feeding, toileting, and moving around when you are severely disabled. Severe disability can unexpectedly happen like a stroke or serious accident. It could also be caused by progressive worsening of chronic conditions such as diabetes or frailty due to old age.

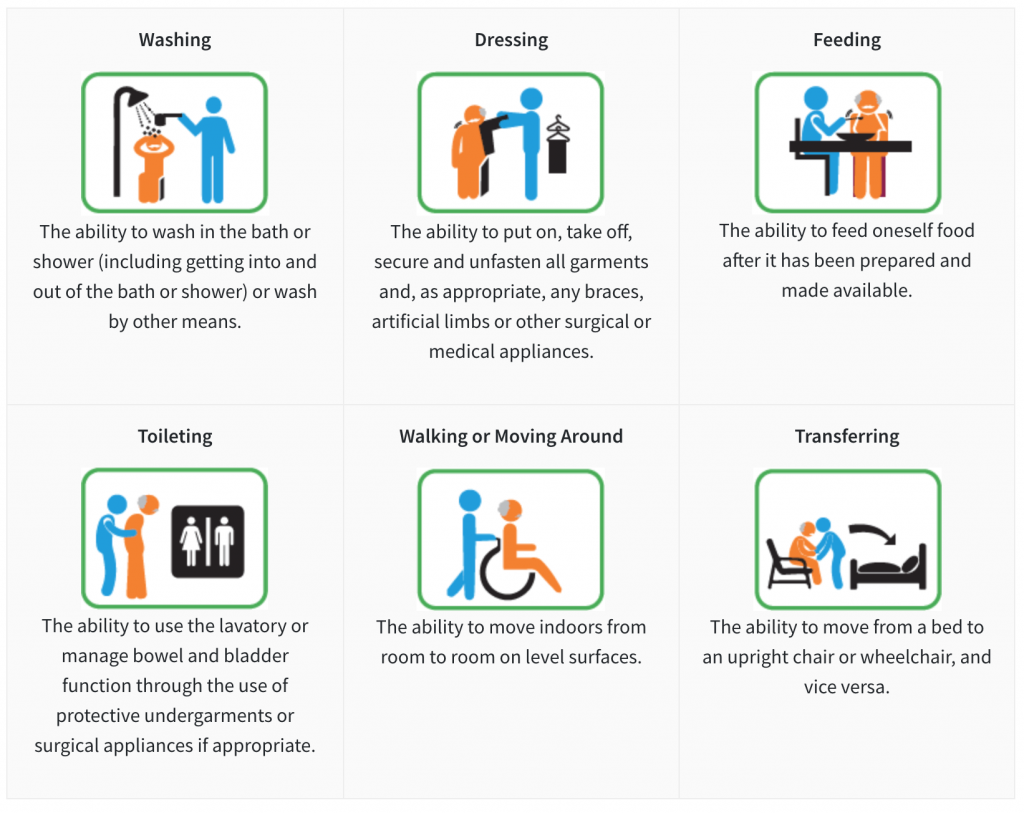

Long-term care insurance provides financial support should one become severely disabled and need personal and medical care for a prolonged duration. Severe disability refers to the inability to perform at least 3 of the 6 Activities of Daily Living (ADL).

These 6 ADLs are:

Sources: Ministry of Health Singapore, Aviva

The question on many younger Singaporeans’ minds is “Why make CareShield Life compulsory?”. My reply is because the need is real.

Though health issues like stroke, cancer, and heart disease are more prevalent in the advanced years of life, there is no denying that a severe disability can happen to anyone, regardless of age.

According to statistics cited by Health Minister Gan Kim Yong:

- 50% (or 1 in 2) of healthy Singaporeans aged 65 years are expected to become severely disabled in their lifetime.

- To add to this, Singaporeans are also living longer and healthcare technology is only going to improve. The average lifespan of Singaporeans in 2040 is projected to be 85.4 years old (Source: TODAY 17 October 2018, Average lifespan of S’poreans in 2040 will be 85.4 years, third-longest globally: Study).

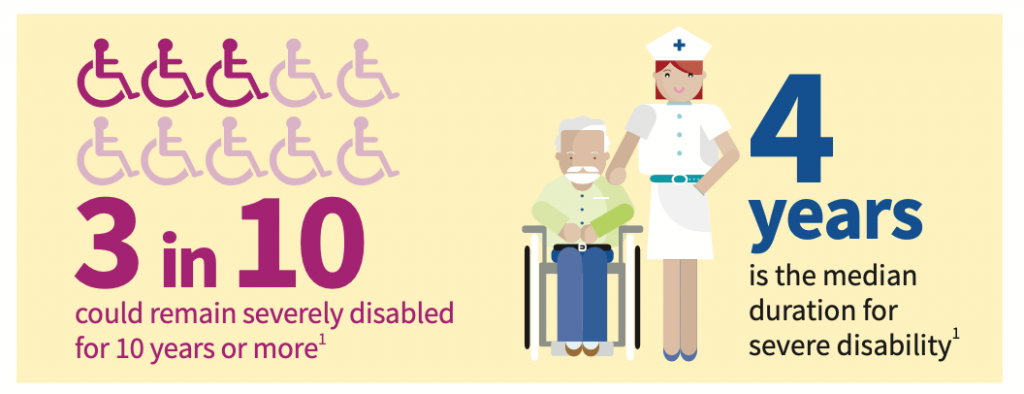

- It is also estimated that 3 in 10 remain in severe disability for 10 years or more (Source: Ministry of Health on CareShield Life, updated 22 November 2019).

Source: Aviva

Will our retirement fund last us for 10 years or more should we become severely disabled? If that day really comes, would we have enough for food, utilities, housing loan, daily necessities, and medical bills? Getting a trained helper, nurse, or even nursing care services all require money. And the reality is long-term care can be costly and prolonged! The monthly estimated expenditure will increase, yet income would be next to nothing.

Young people often think that severe disability is a remote possibility. I was no different from them at that age. However, increasingly, we hear more about how young people, as a result of accidents or illnesses, suffer from long-term disability. It is challenging – physically, emotionally, and financially – for the person suffering from disability and his or her family.

By having adequate coverage for your needs from your 30s, you will have fewer worries about long-term care financing, whether you suffer from a severe disability during your productive working years or retirement years.

Before we look at the costs involved, let’s understand the features of this new scheme.

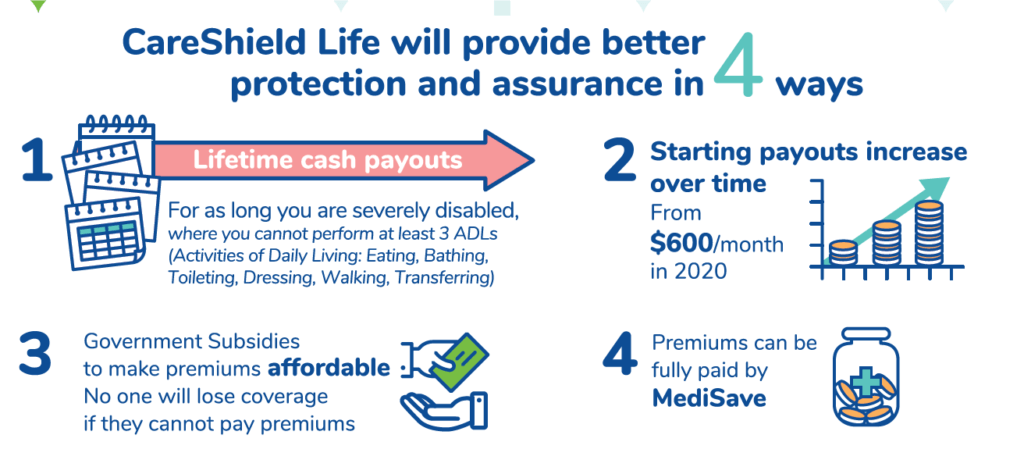

Key Features of CareShield Life

- Lifetime monthly cash payouts, for as long as the insured remains severely disabled

- Criteria for the claim: Inability to do 3 out of 6 Activities of Daily Living (ADLs)

- Increasing payouts i.e. at 2% per annum starting at $600/month until age 67 or when you make claims, whichever is earlier. This is a valuable feature as inflation devalues our money. For example, a 30-year-old policyholder at scheme launch in 2020 becomes severely disabled 1 year, 25 years, and 37 years later:

- At age 31, the fixed payout will be $600 per month for life.

- At age 55, the fixed monthly payout will be $1,000 per month for life.

- At age 67, the fixed monthly payout will be $1,200 for life. Note that actual payouts will vary depending on regular adjustments based on longevity and disability trends.

- Premiums are based on a 2% increment rate for the first years i.e. between 2020 to 2025. The rate at which it will increase in subsequent years will be decided by an appointed council. Factors affecting the rate of premium increase include claims trend and inflation.

- Premiums can be fully paid by Medisave

- Premiums begin from age 30 to 67 (or current re-employment age whichever is higher)

- Unlike ElderShield, which was administered by private insurers, CareShield Life will be administered by the Singapore government. MOH has highlighted that its underwriting process for CareShield Life would be more inclusive. Every person who is not severely disabled can join CareShield Life in 2021.

Note:

- Once an individual starts collecting a payout, this amount will be fixed for the person and will not increase, even when the scheme’s payout increases in the future.

- Similarly, the payout amount will be fixed at the amount the year an individual pays the last premium at age 67.

How Much Does Long-Term Care Cost in Singapore?

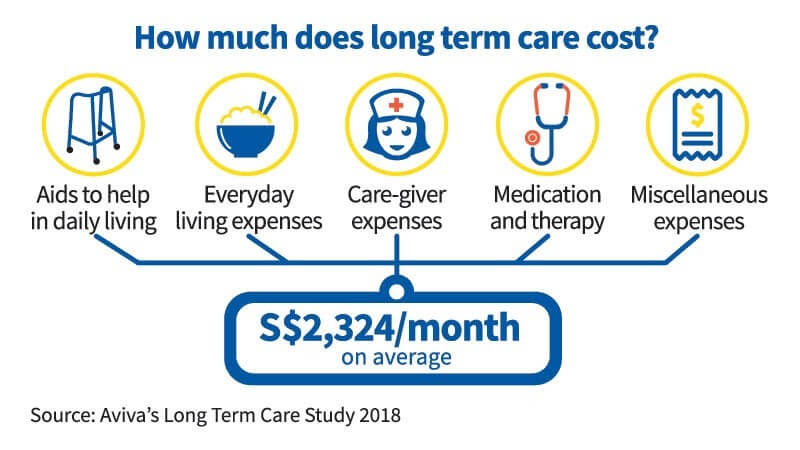

According to Aviva’s Long-term Care Study 2018, the average cost of long-term care is S$2,324 per month.

Can you afford an additional $2,324 every month on your long-term care? This amount can potentially wipe out all your savings! This is why it is critical to plan for long-term care financing. I am glad the Government studied the facts and recognized that there is a need to extend compulsory long-term care protection to the younger generation. CareShield Life serves to mitigate some of the costs.

How Can CareShield Life Help in the event of a Severe Disability?

CareShield Life will provide lifetime cash payouts to help cover some of the costs of long-term care in the event of one’s inability to perform 3 out of 6 ADLs. The cash payout starts from $600 per month and will increase at a rate of 2% per annum over time. This is to keep pace with inflation.

Is this sufficient? It is a resounding no!

This amount is clearly insufficient to meet the average cost of long-term care in Singapore. But it does provide some basic financial support for the majority of Singaporeans and PRs. Those who wish to enhance their coverage to get higher monthly payouts can apply for a CareShield Life Supplement offered by private insurers (Aviva, Ntuc Income, Great Eastern).

One noteworthy point about CareShield Life is this – it provides universal coverage for all. This means that those with pre-existing conditions and disabilities will also be covered.

What About Premiums?

Based on your age in 2020, you can expect to pay between $206 to $366 a year for CareShield Life. Since this is a national scheme, premiums are fully payable by Medisave and the Government will also provide transitional and means-tested subsidies to make premiums affordable. To calculate your premium, you can check out the online premium calculator on the MOH website.

How Do I Go About Applying for CareShield Life?

Well, you will be automatically enrolled in CareShield Life. As the first cohort, by now, you would have been notified by the Government of the policy commencement date which is 1 October 2020.

For those age 40 and above in 2020

You may be wondering how CareShield Life will affect you and whether you should switch to CareShield Life.

Coming up next, check out my article “How Does CareShield Life Affect Me? Should I Switch to CareShield Life or Stay Put with ElderShield?” to learn more.