Karen Tang, CFP®: Certified Financial Planner in Singapore

9 out of 10 people I speak to have not heard about Disability Income Insurance (DII).

They assume that Total and Permanent Disability (TPD), which almost all of them have in their life coverage, is the blanket disability definition across all life insurance products. But they are wrong.

Many folks have different enhancements (i.e.riders) to TPD like Enhanced TPD, Deferred TPD in their insurance policies but they do not necessarily understand exactly what these do for them. And these enhancements are certainly not the same as the claim definition for disability in a Disability Income plan.

These riders typically refer to how the benefit will be paid out, for example, the number of installments and the number of years payment will spread out. In some cases, it is a lump sum. Insurers have also capped the total aggregate payout for TPD to $X million (so buying in excess is not necessarily a good thing).

Yes, you have TPD coverage but what is the probability of you making a successful claim for it?

What is Total and Permanent Disability (TPD)?

First, you need to understand the difference between TPD and the definition of disability applied in Disability Income Insurance.

The definition of Total & Permanent Disability (especially in older life policies) refers to:

- Total and irrecoverable loss of the sight of both eyes or loss of sight of one eye and loss by severance of a limb or loss by severance of a pair of limbs.

- This, to me, is a stringent criteria to fulfill. Some insurers, on the other hand, include a definition of ‘loss of use’ and not just ‘physical severance’.

To date, some insurers have also included ElderShield Activities of Daily Living (ADLs) into its TPD definition.

- For example, a TPD payout is admissible if “as a result of disease, illness or injury, accident the life assured becomes totally and permanently unable to perform at least 3 out of 6 ADLs even with the aid of special equipment and always requiring physical assistance of another person throughout the physical activity for a continuous period of 6 months”.

- This, I would say, is more lenient than the TPD definition.

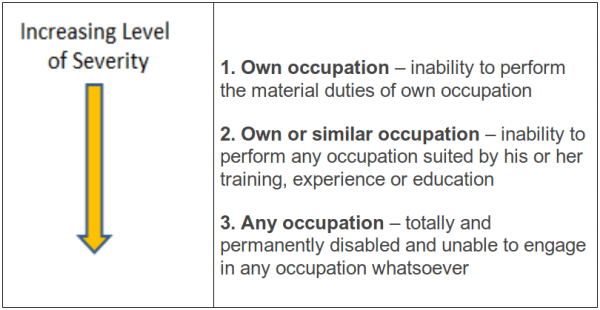

What then is the definition of disability in Disability Income Insurance (DII)?

The definition of disability in DII is tied closely to one’s ability to fulfill the material duties of one’s occupation. Here are the different types of disability and their corresponding severity levels:

Analysis of the Levels of Severity

- As you can see, there is a huge difference between ‘own occupation’ and ‘any occupation’. The latter refers to a situation whereby the individual is incapable of performing any work to earn a living.

- TPD coverage provides for the most severe form of disability where one cannot earn any income at all and such a condition must be diagnosed as permanent, or if the person loses the use of any two of his eyes and limbs (severity level 3).

- For severity levels 1 & 2, you need not lose an arm or leg or eyes to be compensated. As long as the disability resulting from an illness or accident renders you incapable of working to earn an income, you will be paid the monthly benefit (the insurer will have its own formula in deriving your maximum monthly income benefit). Insurers generally do not publicise their claim statistics but one insurer revealed this – in the month of Dec 2009, the total claim amounted to $9,294,074.00 for life insurance of which $265,138 was paid out due to TPD. This translates to only 2.9%!

Other things to note for Disability Income Plans

- Some plans also pay for partial disability i.e. your condition has improved and you are able to return to work but at a reduced capacity (eligible benefit is based on a formula specific to each insurer).

- Benefits, terms and conditions do vary between insurers (only 4 insurers in the market this product) so be sure to understand them before making a commitment.

- Some Disability Income Insurance are sold as a standalone plan while others are riders attached to a main plan.

Final thought

The level of awareness of DII is low as compared to other life insurance products as not all insurers carry DII and insurance agents prefer to sell whole life, endowment and ILP products for obvious reasons. Well, my readers, do not be deceived by ‘fancy’ TPD rider names – seek qualified and comprehensive financial advice to protect your best interests.

A real life story:

Here’s a real life story of JJ who would have benefited from Disability Income Insurance.