As I have shared with you in my earlier post, claiming from Disability Income Insurance (DII) is less stringent than from a plan with a Total and Permanent Disability (TPD) definition (loss of use or physical severance).

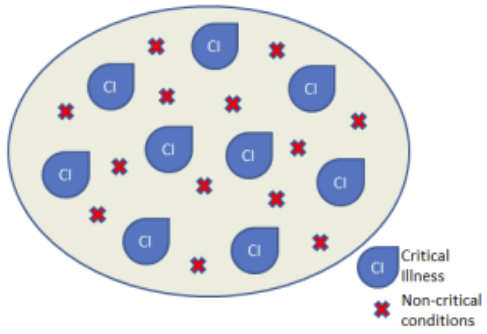

What you may not know is this – there are conditions that can incapacitate you from working and they need NOT be a critical illness or a TPD.

Disability Income Insurance – Filling the Gap

Let me put it this way – conditions that fall through the ‘crack’ (i.e. do not satisfy the definitions of critical illness or TPD) in a life insurance policy could potentially fulfil the definition of disability in a Disability Income Insurance plan.

Non-critical conditions could include mental, psychological and orthopaedic issues. A note about major depressive disorder or depression:

- In Singapore, depression is one of the top 3 mental illnesses (Source: Institute of Mental Health media release 18 Nov 2011: Latest study sheds light on the state of mental health in Singapore.).

- The report states that 5.8% of adult population in Singapore suffered from depression at some time in their lifetime.

- Fast forward to 2017, the New Paper dated 06 Feb 2017 published an article titled “Depression can hit anyone, Kids as young as 10 suffer from it; women and people living alone at higher risk”.

- The statistics remain unchanged – Depression is still one of the top three mental health disorders here, according to a National Mental Health Survey conducted by the Institute of Mental Health

If you value your greatest asset, that is, your ability to work, then Disability Income Insurance ought to be a pre-retirement essential in your insurance portfolio. The coverage duration could be up till age 55, 60, 65 or even 85.

I was again reminded how vital it is to protect our ability to earn an income. Here is the situation of a friend which I’d like to share with you.

I caught up with JJ in Dec 2017. He worked as a CPA with one of the big four firms in Singapore.

JJ, age 45, suffers from Chronic Inflammatory Demyelinating Polyneuropathy (CIDP). He was diagnosed 5 years ago.

- It is an acquired immune-mediated inflammatory disorder of the peripheral nervous system and it is a chronic disease (not a critical illness).

- CIDP is believed to be due to immune cells, cells which normally protect the body from foreign infection, but here they begin to incorrectly attack the nerves in the body instead.

- As a result, the affected nerves fail to respond, or respond only weakly, to stimuli causing numbing, tingling, pain, progressive muscle weakness, loss of deep tendon reflexes, fatigue, and abnormal sensations.

- The likelihood of progression of the disease is high. There is no known cure.

- Ongoing treatments include plasma exchange and intravenous immunoglobulin which may be prescribed alone or in combination with an immunosuppressant drug.

A guy known for his good physique is now a scrawny chap who is incapable of working a job. My heart goes out to him … he is uninsurable (insurers rejected him totally). At 45, he has no livelihood, depending only on his wife’s income.

Too late …

His insurance agent, unfortunately, did not recommend him to take up disability income protection. His existing insurance coverage did not pay a single cent for CIDP. What was even worse was that when he was about to upgrade to a comprehensive ‘as charged’ integrated shield plan, JJ was diagnosed with the disease and the insurer rejected his application. He will be facing some huge hospital bills in the years to come.

Food for thought

Life is unpredictable! Do not procrastinate any longer – beef up your financial planning in areas where you need to. If you are not under the active care of a CFP® representing a comprehensive financial advisory platform or have not reviewed your financial holdings in the past one to two years, perhaps it is an appropriate time to do so now.