Karen Tang, CFP®: Certified Financial Planner in Singapore

Do You Have Adequate Critical Illness Insurance?

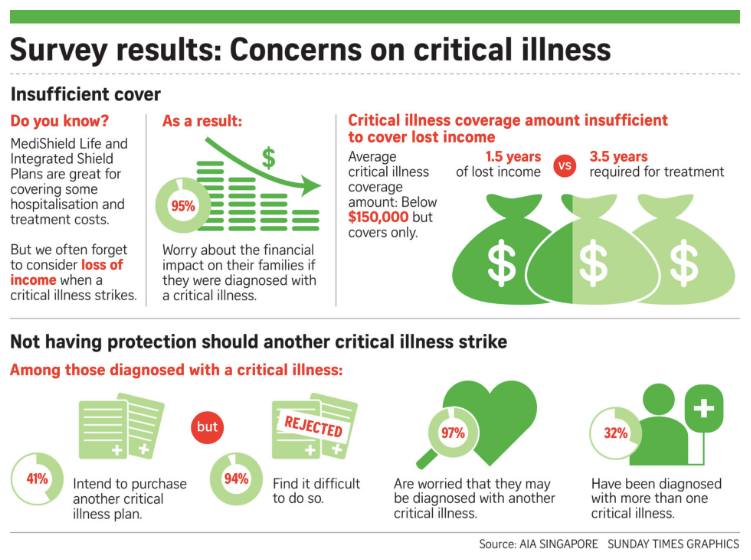

The Straits Times published an article “AIA survey uncovers 3 gaps in CI coverage here” on 22 August 2016.

I am not surprised at all by the survey findings. In my decade long financial planning practice, I have not met any client who has secured adequate critical illness coverage.

Some of the insurance portfolios I have examined are skewed towards endowment (savings) plans and Investment-Linked Policies (ILPs). Different types of insurance have different purposes. And it must be reiterated that saving plans do not equal protection. This is because such plans usually provide coverage for death but not total and permanent disability (TPD) or critical illness (CI).

As for ILPs, the truth about escalating mortality charges (i.e. cost of insurance) is never explained to customers at point of sale. The ILP can lapse around one’s retirement years and one can lose insurance coverage when one needs it the most!

Gap #1: The average coverage amount is insufficient to cover loss of income and other relevant costs.

My comments:

First thing first – Critical illness protection is CORE in insurance planning. When I look at an insurance portfolio, the area that I zoom in on first is the critical illness coverage. Whether the individual is a swinging single or a breadwinner or a double income couple with no kids, there must be adequate critical illness coverage. And before I commence on any planning work, I will share with my client the insurance planning framework that I use and the various pre and post retirement essential components that will form a robust and foolproof protection program.

GAP #2: Singaporeans are concerned about not having protection should another critical illness strike.

My comments:

This is a very real concern! With statistics revealing that almost one in three (33%) of the surveyed are already diagnosed with more than one critical illness, it should make us all rethink and reexamine our critical illness protection.

GAP #3: Singaporeans seeking protection for more critical illness conditions across different stages.

My comments:

Critical illness coverage has, for the longest time, been synonymous with covering only advanced or late stage conditions. It is good news that more and more Singaporeans are aware of early and intermediate stage CI coverage. Being informed means that proactive action can be taken to close the gap.

Limited pay whole life plans and term plans these days are getting more sophisticated in their scope of coverage. A comprehensive whole life or term (by attaching appropriate riders) plan can cover early, intermediate and advanced stage illnesses, accidental death, disability income and special conditions like osteoporosis, osteoarthritis, diabetic complications and even juvenile related ones.

More and more people want to be covered for early and intermediate stage illnesses. For those who are diligent with their annual health screening, they would stand to benefit more from such protection plans.

Food for thought:

- Do a financial planning review today! If you wish to get a second opinion from a comprehensive financial planner, feel free to contact me.

- Get insured while you are still healthy! It is good to have some coverage than nothing at all.

- It is better to have more (if you can afford it) than less. Because no one will complain of having too much insurance payout when you need it the most!

- Look after your health because no one has more vested interest in it than yourself.