Karen Tang, CFP®: Certified Financial Planner in Singapore

Most investors face a dilemma in correct decision-making: when to buy, when to sell, what to buy, what to sell, how much to buy or sell, and at what price!

What if I told you that there is a way by which you could take profits when markets are high, and invest when prices are low – automatically?

Luckily, there are ways that can help you WIN as a “passive” or defensive investor.

How is that? I will show you.

Once you have done your financial planning with a qualified consultant, you will know how much money you have left to invest, and your risk profile.

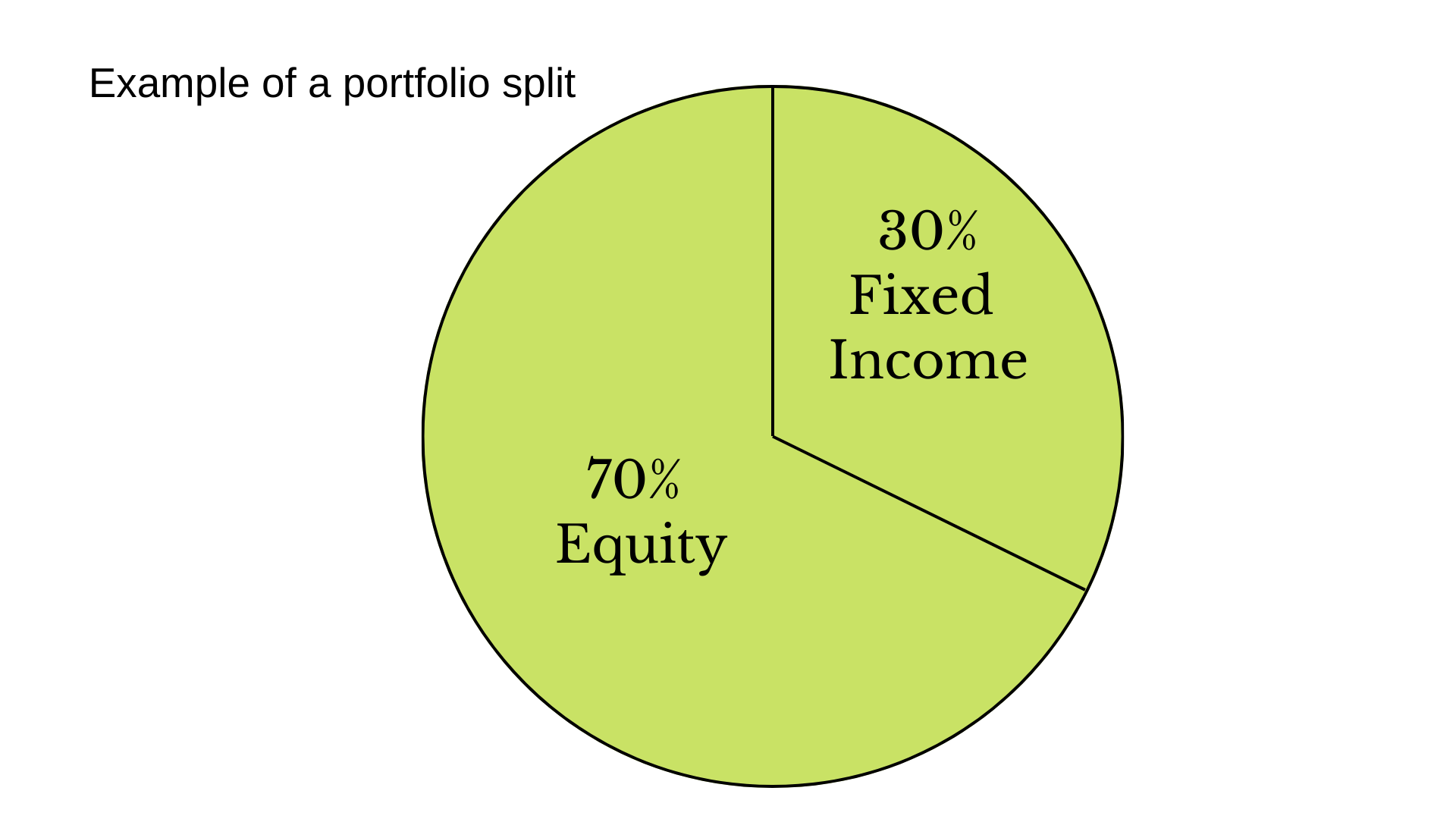

Let us start with what your ideal financial investment portfolio looks like. What is the split i.e. ratio of the asset classes? No matter how large or small the absolute dollar value is, it is wise to think of it in terms of percentages.

The main two asset classes are equity a.k.a. common stocks i.e. shares of publicly traded companies, and fixed income a.k.a. bonds. These two asset classes complement each other very well.

How do you rebalance or reset the portfolio allocation?

Consider a balanced portfolio which has 50% each of bonds and equities. All you have to do is reset this balance every year on the same date.

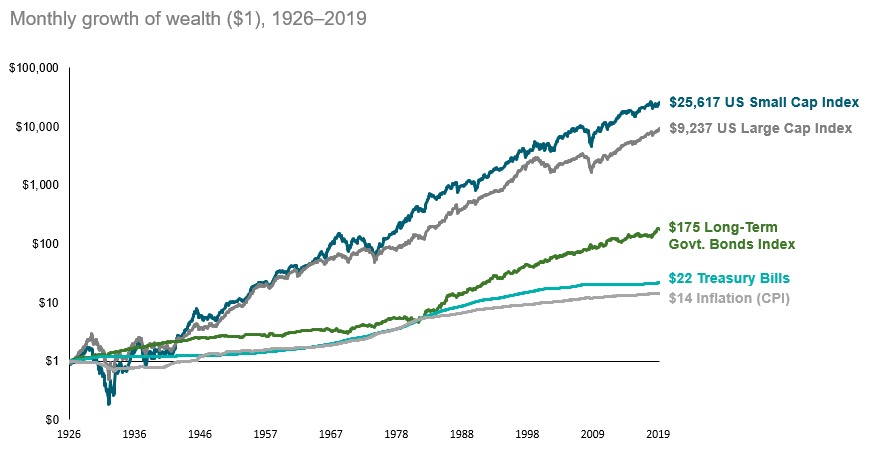

Equities give us great returns over the years, usually well above inflation, especially if you reinvest the dividends.

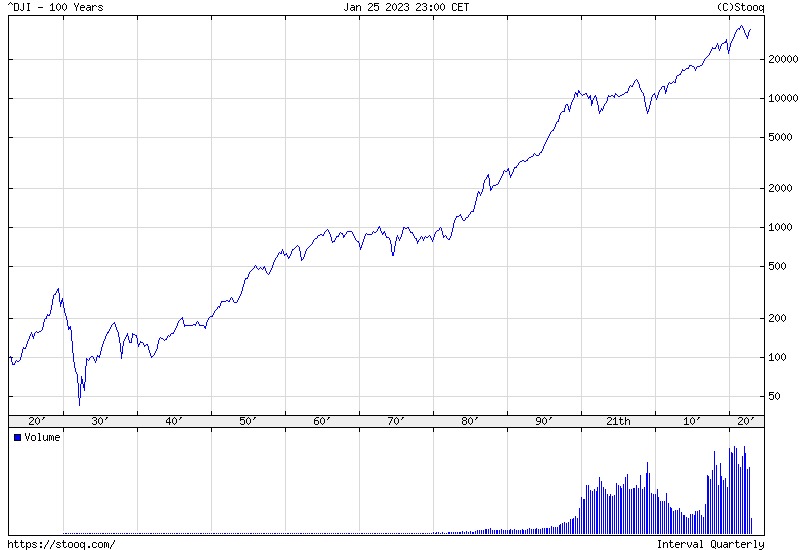

Chart 1: 100-year logarithmic chart of US Dow Jones index 1923 to 2023 shows a run up in spite of a world war and many other doomsday scenarios.

The downside with equities for some investors is that they can be volatile in price from day to day. It is almost as if the markets are fickle and tend to overreact, oscillating from one extreme to another in the short term. This volatility is seen by some as “risk”, but in reality it can be taken advantage of, as we will see later in an example below.

Chart 2: Dow Jones Index – 1 month shows some ups and downs.

Bonds on the other hand are considered more “conservative” because they are much more stable, but offer lower returns than stocks.

Chart 3: Bonds rise more slowly, but with a lot less volatility compared to equities. This volatility is the risk that some investors want to avoid.

Now, suppose you as an investor, after having done proper planning and knowing your risk tolerance, decide that you are good with a 50/50 balanced portfolio. A balanced portfolio typically consists of 50% stocks and 50% bonds.

Equites can be represented by a basket of well-chosen, actively-traded, low-cost, globally diversified unit trusts or index tracking funds. This is to ensure they are quick & easy to buy and sell (a feature known as liquidity). Diversification also reduces risk. In our example today, we will take a low-cost US S&P 500 index tracking fund such as by Fidelity or Vanguard to represent the equities component of the portfolio.

The fixed income portion of our portfolio is represented by investment-grade bonds or bond funds.

Example:

We start with $1000 with $500 each in equities and bonds.

In your investment plan, you decide that you will rebalance this ratio in your portfolio every year on 1st July.

The beauty of rebalancing is that if one year the stock markets rally up, we sell some stocks which are relatively high in price and put it into bonds.

Another year, if stocks go down, we simply take some money from the bonds side and put it into stocks while they are cheap.

With this, we are able to sell when expensive, buy when cheap – without thinking.

Now, if the stock markets go UP a lot next year, when equities rally 24% and bonds give us a modest 4%. We now have $620 in equity and $520 in bonds, for a total of $1,140. To arrive at a 50% split of $570 each, we need to sell $50 of equity and put it into bonds.

The vice versa can be done when stocks underperform. Though in most years, stocks will tend to rise much faster than bonds. We typically see many more years bullish i.e. rising stock markets, with a few years bearish i.e. falling prices. This system, which we call “magic portfolio” takes advantage of these disparate ups and downs of the two asset classes. Also, due to the fact that the portfolio has sufficient bonds, its value will fall much lesser than the broad stock market during bearish times.

Best of all, it removes the confusing issue that investors face about “timing” the market. We don’t need to read the news endlessly and follow TV pundits.

This makes rebalancing a very important tool or habit for investors.

Another similar practice: Periodic realignment

This is where the investor creates a fresh portfolio every year or two and “realigns” their current holdings to match the new, well-researched portfolio allocations appropriate for the present time.

This is so that the portfolio remains “fresh” and we do not keep holding on to old assets – which could be winning or losing – because of unwise emotional reasons.

The aim is to hold only those assets which we would buy with our money today. But at the same time, we do not want to (have the pressure on us to) make random, ad hoc decisions with our money.

Good, conservative investors sleep well at night. Peace of mind is one of the main aims and advantages of value investing because it is based on sound assumptions, expectations, and logic.

Why Your Friend in Finance Should Not Plan Your Finances

In my more than 15 years of financial advisory practice, I noticed that many successful people still handle money in an informal way. Instead of

Micro-Retirement: Rethinking Work, Money, and the Pace of Life

Recently, I was introduced to the concept of micro-retirement, that is the idea of taking intentional, extended breaks from work, ranging from a few months

Contributing to the Supplementary Retirement Scheme (SRS)? Here’s What You Need To Know

It’s the ‘SRS rush’ season once again. You have just about 3 weeks left to contribute to your Supplementary Retirement Scheme (SRS) and enjoy tax